When you’re choosing an equity market allocation I generally prefer to keep things simple – just buy a low fee global market cap weighted portfolio and call it a day. If you build your hedges (bonds or whatever) around that slice correctly then your asset allocation will match your risk profile and you’ll have a reasonably good probability of having constructed a plan that you’ll stick with and will work just fine for you over long periods of time.

One of the reasons why I like a market cap weighted stock allocation is because it’s a momentum strategy. Now, don’t get me wrong. I’ve been pretty clear that I don’t love factor investing. But momentum works for a fundamental reason – it’s the natural evolution of creative destruction. You could say that all market cap weighted index funds are momentum funds because they more or less reflect the process by which corporations succeed and fail.

The S&P 500, for example, is a momentum strategy. It’s a simple low fee market cap weighted momentum strategy. The reason most more active managers can’t beat it is because they are less tax and fee efficient and don’t benefit from the economies of scale that the S&P 500 index does. But the kicker here is that if you look under the hood the S&P 500 is just a big momentum strategy that systematically sells losers and buys winners. It does this by creating a rules based system for inclusion in the index. When a company doesn’t meet that standard the index committee chooses to sell it and replace it with a company that meets their criteria.

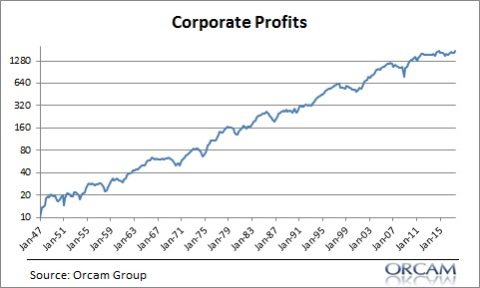

The primary reason why this works so well is because it is a systematic way of aligning yourself with the success of corporate America over time. Corporate America, after all, is a big momentum machine that systematically kicks out inefficient entities so that newer more efficient entities can take their place. As consumers we tend to spend a little bit more money each year in a systematic manner and that growing monetary pool gets spent across an ever changing group of companies who compete for that money. This shows up in corporate profits in what looks like a big stream of profits with ever increasing momentum.

If you look at a chart of corporate profits you can basically see what the S&P 500 is doing – it’s systematically attaching itself to the stream of corporate profits over time because it’s removing failing firms and replacing them with firms that are capturing that market share.

I guess we’re all momentum investors. Although I’d argue that some are smarter than others. Market cap indexing just so happens to be a very low fee and tax efficient form of momentum investing.

NB – I know I am bound to field a bunch of emails and comments from people who love factor investing and swear by it. That’s fine. Look, there’s far worse ways to invest. Hedge funds and c-share mutual funds are still a thing, after all.¹ But I remain skeptical of the factor sales pitch. It just strikes me as unnecessary complexity in a financial world that is complex enough as it is.

¹ – I tease. Some hedge funds and mutual funds are just fine, but this is a blog post and so I’m painting with a broad brush.

Update – I figured many of the factor proponents would hate this idea. The primary pushback has referred to the fact that the S&P 500 doesn’t actually have any exposure to the Fama/French concept of momentum. This is true in that the 12 month momentum factor won’t appear that relevant in the S&P 500 when defined by those parameters because the S&P 500 is approximately “the market” within those parameters. This is a fallacy of composition though. The S&P 500 is not “the market”. The Global Financial Asset Portfolio is “the market”. When compared to the GFAP some degree of momentum will be apparent depending on your parameters for the concept.

Additionally, momentum is a fleeting concept. Momentum is not a static concept and many momentum funds use different measurements because the academic concept is not consistently attainable. Some of the largest momentum funds in the world actually have little exposure to the momo factor as defined within the academic literature which proves how hard it is to put theory into practice. That said, it is not macro consistent to argue that the S&P 500 doesn’t have momentum. At the macro level it is the very definition of something with momentum because it sheds losers and buys winners. We can whittle that definition down into more specific time horizons and crunch data that matches a certain parameter for “momentum” but that’s changing just the parameters and fixing the taxonomy to match data that may or may not be captured in the future.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.