I was disappointed to read this Wall Street Journal article about Bill Miller’s mutual fund performance painting the fund as some sort of superb performer. Yes, it’s true, the nominal performance of the Legg Mason Opportunity Fund has been tremendous over the last 3 years. The article notes that the fund has “trounced” the S&P 500 in the last 12 months and outperformed 97% of funds in its category over the last year. But this looks like a case of bad benchmarking and erroneous performance analysis. Let’s explore why:

- First, the Legg Mason Opportunity Fund is a fund with 57% of its portfolio invested in micro-caps, small-caps and mid-caps. It is NOT comparable to the S&P 500 which is entirely comprised of large cap stocks. So comparing it to the performance of the S&P in the last 12 months is irrelevant.

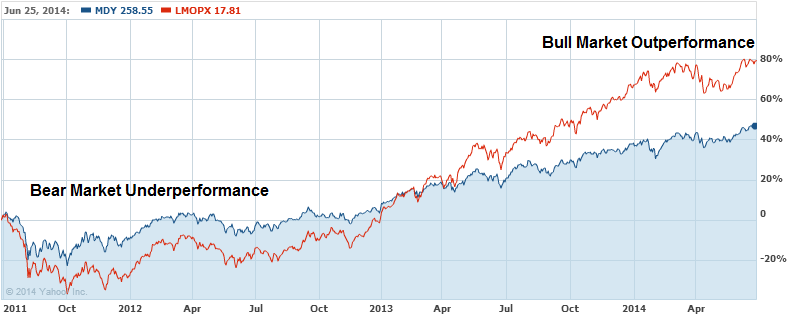

- Second, because the fund is comprised of many high beta stocks it is therefore much more volatile than the S&P 500. In fact, it’s even more volatile than its proper benchmark, the S&P 400 midcap fund. This can be seen over the course of the fund’s 3 year performance during which you can clearly see how the fund underperformsn in a bear market environment (like the summer of 2011) and outperforms in the subsequent bull market:

- Lastly, when we run a basic risk adjusted return analysis the fund performs exactly how we might expect – it has a standard deviation of 24.8 and a Sharpe ratio of 0.95 over the 3 year period. And the S&P 400 midcap Index has a standard deviation of 17.8 with a Sharpe ratio of 0.92. In other words, they are virtually the same fund over this period except the Opportunity Fund charges a net expense ratio of 2% relative to the expense ratio of 0.09% for the Vangaurd Midcap ETF.

There’s no doubt that the Legg Mason Opportunity Fund has turned in tremendous performance over the last 3 years. But the praise of this fund during the recent bull market appears to overstate how beneficial this performance has really been relative to a proper benchmark. It’s true that this fund might be proper for some portfolios, but the decision to invest in this fund and any fund should first entail proper fund evaluation. Unfortunately, these types of articles drive money into funds that may not be totally appropriate for investors because they misconstrue how a fund is benchmarked and how its performance should be analyzed.

Related:

Pragmatic Capitalism: What Every Investor Needs to Know About Money and Finance

What is the Biggest Mistake When Analyzing Funds?

Can we all agree to stop Comparing Everything to the S&P 500?

Why do Investors keep Buying “Actively” Managed Funds?

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

Comments are closed.