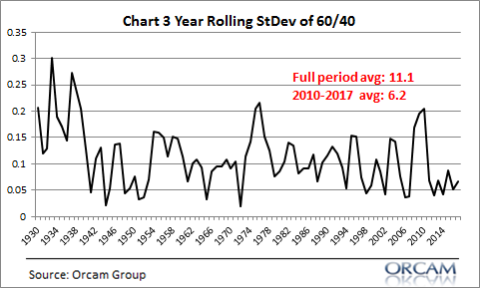

So, the market’s finally gotten a little interesting. It’s been a while. I feel like we’ve been sleepwalking through years of stable and steady market returns. In fact, the last few years have been unusually stable. The 3 year rolling standard deviation of a 60/40 stock/bond portfolio has been just 6.2 since 2010. The average since 1930 is 11.1. So, we’ve been spoiled by high and stable returns in the post-crisis period and now it looks like the party is ending. But does that mean we should panic and destroy the evidence before mom and dad come home? Let’s think this through before we overreact.

The 30,000 Foot View

My basic macro view is simple – I think the US economy is doing okay. We’re still muddling along, but there are no huge red flags out there. There are pockets of housing that are bubbly, but it’s nothing close to 2006. And the banking system is much healthier. So some correction in places like San Francisco, Seattle, Austin and other booming cities could be a welcome development. Of course, if you subscribe to the theory that housing is the economy then this will have at least some meaningful impact on GDP. It could even be enough to drag us into a minor recession. But the macro risks in real estate are nothing like they were before the GFC so let’s not blow this out of proportion.

As for other segments of the economy – there’s legitimate worry about some excesses in the tech sector and the growth in corporate debt. The energy sector is clearly sluggish as oil prices crater. But this looks more foreign demand driven than domestic. So there’s pockets of risk in the US economy, but nothing that looks to me like a widespread macro risk like the way things looked running up to the GFC.

The foreign picture is less certain. Europe is, well, Europe with their half constructed monetary union and Brexiteers. And China is, well, who the hell knows. And that’s actually a legitimate worry. I am waiting for the day when China sneezes and the world catches a cold. And since the Chinese economy is so opaque there’s a real worry that something could be happening over there that catches us off guard. Still, the US is somewhat insulated from recessions in China, but a GFC style event in China would certainly reverberate around the world. And I won’t even begin to pretend to know whether that’s happening right now or not.

Related to that is Trump’s trade war. I haven’t been all that critical of Trump’s policies because I tend to think that people overstate the impact of the President and public policy (with the exception of recessions and financial panics – I think the government multiplier is much more significant in those environments). But Trump’s trade stuff is seriously stupid. He somehow managed to take the only thing that all economists agree about and go against it. And while the tariffs haven’t been substantial so far, there’s no way of knowing how all of this reverberates through the global economy. I can’t imagine it’s good and if we’re to believe FedEx and their last earnings statement then this is an own goal that is colossally stupid. I mean, an own goal like the kind where the goalie picks up the ball and just throws it into his own net – that kind of stupid.

So, long story short – domestic economy looks okay-ish, foreign economies not so hot and China could be blowing up or booming and no one will know until the Chinese decide that they want to let us all in on the secret. All in all, it’s kind of more of the same with an outlier risk that China is entering a big downturn. But since domestic recessions are usually when the stock market gets pulverized we can argue that a 50% decline type of environment is a low probability outcome. At least for now.

What About the Financial Markets?

My view on the financial markets hasn’t changed much in the last few years. All the evidence points to lower future returns that are consistent with a stock bull market that is long in the tooth. As I’ve noted on many occasions, the likelihood of lower future returns is high. Years like 2018 are why I am an advocate of countercyclical indexing – most people should index, but they need more risk management than “buy 60/40 and think long-term”.

Think about it like this. The current yield on an aggregate bond index is 3.25%. You’ll have trouble beating that in the bond market in the coming 5 years without taking a lot of risk. I like to think of the stock market as a high quality 7% yielding long-term bond that occasionally gets overpriced and underpriced (thereby generating lower and higher future returns as multiples expand and contract). Typically, when multiples are high this is indicative of an environment where we’ve earned more than that 7% and some mean reversion is probable. And vice versa.¹

Today is consistent with the type of environment where stocks have earned more than that 7% and multiples are high. And if you get some mean reversion then we are likely to earn less than 7%. So, let’s just generalize and assume we get 5% in stocks and 3.25% in bonds over the next 5 years – well, a 60/40 stock/bond portfolio will mean 4.5% annual returns. Not terrible, but not great. The path to getting there is trickier. My guess is that multiple contraction means more bumpy years like 2018 intermixed with pretty good years. In other words, the path forward isn’t going to be nearly as smooth as the last 8 years.

Conclusion

The bottom line is that things don’t look great. But this also isn’t the second coming of the GFC. We shouldn’t be surprised that the stock market doesn’t go up every year and in fact, we need it to go down sometimes so that it can sustain the ups.² At the same time, the financial markets aren’t situated to generate the types of returns that people are used to. So you’re probably going to need to hold onto your butt and be a little more patient than you want to be. So don’t hit the eject button. A diversified portfolio of stocks and bonds might not be the sexiest thing in the world right now, but the patient investor with a good plan should beat the rate of inflation over time if they focus on what they can control (their own behavior, taxes and fees) rather than what they can’t control (the financial markets).

¹ – I used 7% because it’s close to the average historical rate of corporate profits. General, I know, but there’s no such thing as being precise when we’re trying to guess the future.

² – Most investors hate volatility, but volatility is part of why we’re able to generate higher future returns. Volatility, after all, reflects the uncertainty with which corporations engage in profit seeking innovation. Volatility, in essence, is the reflection of creativity and innovation that manifests itself as future cash flows. If we want that higher return we have to also want that volatility. One does not generally exist without the other.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.