Jesse over at Philosophical Economics has written a couple of really fantastic posts (see here and here) on indexing and market efficiency. His basic conclusions:

- The trend in passive investing is sustainable.

- The rise of passive indexing improves market efficiency.

I’ve made the same points in a series of posts in recent months including:

- Passive Investing Isn’t Hurting the Economy.

- What if Everyone Indexed?

- Is Indexing Going to Eat the Financial Markets?

- Dear Hedge Funds, Index Funds Didn’t Eat Your Returns.

Although I’ve written a good deal on this I didn’t explain why indexing has made life so much harder for traditional active managers (aside from the obvious one which is huge hedge fund fees). And although I totally agree with Jesse’s conclusions, I think we disagree slightly on the why.

So, Jesse basically says that indexing removes unskilled players from the overall pool by relegating them to the game of owning specific index funds as opposed to engaging in the pursuit of real security analysis. The result is fewer and fewer highly skilled investors pursuing alpha via security analysis. I am going to disagree there. I think that indexing is raising the aggregate skill level by giving everyone access to sophisticated strategies that better reflect “the market” portfolio.

You likely know from reading this site that true passive indexing doesn’t exist. We’re all active because we all deviate from global cap weighting. In addition, we know that an “index” is an extremely vague thing in the modern financial world. Dr. Andrew Lo even wrote an entire paper on this topic because the concept has become so opaque in a world where there’s an “index” for everything from volatility, to futures contracts, to hedge funds and even Millennials. So, we’re knee deep in word games before we can even finish the term “passive indexing”….

That doesn’t matter though. What I want to emphasize is that the rise of indexing (regardless of how “active” that index is) has created products that give even the most novice investor access to more sophisticated strategies. Indexing doesn’t remove unskilled players from the game. It actually brings them into the game in a more even playing field. In today’s world everyone can own Risk Parity, Global Macro, Long/Short, Private Equity, etc. As a result of this product development the overall pool of secondary market investors has become a better reflection of the aggregate financial markets. The result of this is that the swimmers in this pool are all starting to look increasingly similar.

For instance, let’s say we had just two investors in the world. Person A buys all 500 S&P 500 stocks individually while Person B just finished reading some Gene Fama paper and decides to buy just 200 momentum stocks in a product wrapper like an index fund. When the momentum buyer enters the market she will likely change the composition of the S&P 500 because her entrance to the market changes the allocation that Person A owns. As a result of this Person A’s portfolio actually starts to look more like Person B’s portfolio because now her momentum stocks look more momentumy (I just made that word up). Person A’s portfolio won’t be a perfect reflection of Person B’s for obvious reasons, but layer on 10,000 various index funds all trying to capture some form of alpha that doesn’t exist in the aggregate and you get a bunch of portfolios that increasingly look similar.¹

A better (or worse, depending on your view) visual here might be Person B peeing in Person A’s pool. Person A’s pool will absorb the change in color, but it won’t be exactly the same color as before and in the aggregate the pool will morph into some other color reflecting all of the liquid that comprise that pool.

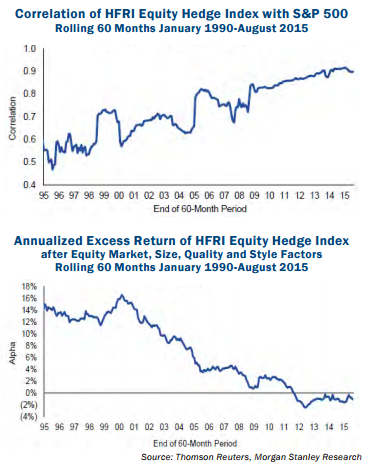

This shift in the financial markets can best be seen in the hedge fund space where the growth in the industry has coincided with rising correlations to the S&P 500 and shrinking alpha. This shrinkage is occurring because the product wrapper we call “hedge funds” creates customized index-like strategies that give more and more investors access to a broader and deeper secondary market. As a result, they all necessarily begin to look like the same thing in the aggregate.

So, the reason that indexing makes alpha more unachievable is due to the fact that indexing makes the participants in the aggregate financial pool appear increasingly similar because they’re all utilizing a more sophisticated approach to asset allocation leading to a more homogeneous reflection of “the market” portfolio. As a result, the margin for outperformance inside of the pool becomes increasingly thin leading to alpha shrinkage.²

¹ – See, Understanding Modern Portfolio Construction.

² – I have significant knowledge in the area of shrinkage in pools so trust my opinion here.

NB – Notice I don’t argue that indexing makes the market more “efficient” as in, it reflects all available information. I don’t know what that term even means in a world where the idea of market efficiency must necessarily be a gray area. I personally don’t find the concept of an efficient market to be all that useful since it is impossible to prove or disprove the idea that “the market” always reflects “the market” accurately.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.