This is the fifth instalment of a ten part series similar to what I did with “The Biggest Myths in Economics”. Many of these will be familiar to regular readers, but I hope to consolidate them when I am done to make for easier reading. I hope you enjoy and please don’t forget to use the forum for feedback, questions, angry ranting or adding myths that you think are important. This is a long one so hang in there or read just before bed as it should put you right to sleep.

If there’s one thing we all seem to understand about bonds it’s that bond prices fall when interest rates rise. So, the natural thinking in a low rate environment is, “rates can’t go much lower so that means bond prices will fall if they rise”. It seems like such a naturally negative asymmetric bet that it scares a lot of people from owning bonds today. There’s only one problem with this thinking – it’s not necessarily right! The correct statement is, if interest rates rise then bonds prices fall in the short-term.

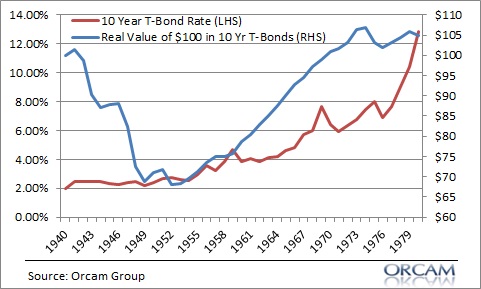

Importantly, there’s a pretty good historical precedent for today’s bond market and a rising rate environment – the 1940’s. In the early 40’s ten year interest rates had fallen to about 2% in the wake of the Great Depression. Bond investors were essentially pricing in a permanent stagnation (sound familiar?). But rates slowly ticked higher and higher until we got to the crazy high rates of the 70’s. But you didn’t lose money holding a 10 year T-Bond during this 40 year rise in rates. In fact, you did quite well in nominal terms:

The story is a bit different in real terms. When adjusted for inflation bonds barely break-even over this same 40 year period:

Although you experienced several real losing 10 year periods during this 40 year period, you didn’t lose money in nominal terms during any 10 year period across this rising rate environment. In other words, if held to maturity you did quite well in nominal terms even if you lost money in real terms. And that’s exactly what we should expect since bonds typically don’t beat the rate of inflation anyhow.

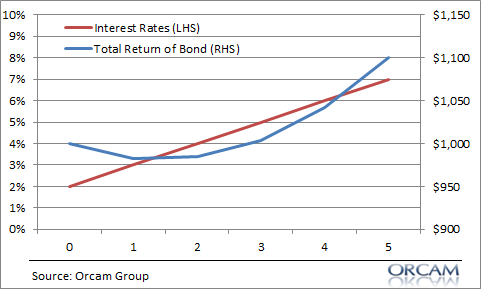

Historical backtests can be unreliable and we shouldn’t let them influence our thinking too much. So let’s look at this from a more operational perspective. Take, for instance, the case of an individual 5 year US government bond with a face value of $1,000 paying 2% per year. If interest rates rise by 1% every year that bond still pays you 2% every year plus you get your principal upon maturity. Here’s how the total return of that bond looks over the course of your 5 years:

If you held on for 5 years you didn’t lose money despite the fact that interest rates rose. In fact, you lost some principal in the first 2 years and then made up for it as the bond reached maturity. This is slightly more complex in the case of a bond fund which is essentially a constant maturity bond, but the same general principles apply.¹ But let’s take a closer look at a constant maturity bond since more and more investors own bond funds these days.

To understand the returns on bond funds in a rising rate environment we have to understand what’s called bond convexity. Bond convexity is a measure of the non-linear relationship between bond prices and interest rate changes. Without getting too deep in the weeds, we should recognize something about bonds – as interest rates rise bond duration declines (bond duration is the bond’s price sensitivity to interest rate changes so, a 1% rise in rates will result in a 5% loss for a bond with a duration of 5). In English, that basically means that a 1% rise in interest rates has a bigger impact on long maturity low interest rate bonds than it does on than it does on long maturity high interest rate bonds. Let’s look at an example here for more clarity.

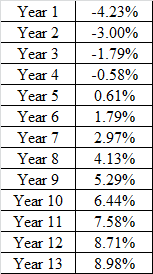

Let’s say you buy a 7 year constant maturity bond portfolio yielding 2% in year one.² Each year interest rates rise by 1% until they reach 15 % like they did in 1981. Remember, this is a crazy extreme example, but useful for illustrative purposes. The image below shows interest rates (the red line) rising from 2% to 15% in increments of 1% per year. The blue line shows the cumulative price (yield plus price change due to interest rate increase) of the 7 year bond portfolio.

What happens here is really important because the constant maturity bond portfolio gets dinged pretty bad at first. I’ve shown the annual price changes at the right. Because the bond is more sensitive to  rising rates when rates are low the 1% increase in rates has a big impact upfront, but then it actually has a positive impact as rates rise. In other words, as rates rise a medium duration constant maturity bond portfolio does not necessarily fall in price. It actually rises in price because the higher interest rate more than offsets the impact of the price decline. This should seem obvious to everyone, but it’s not what we tend to think of when we hear that rising interest rates mean falling bond prices.

rising rates when rates are low the 1% increase in rates has a big impact upfront, but then it actually has a positive impact as rates rise. In other words, as rates rise a medium duration constant maturity bond portfolio does not necessarily fall in price. It actually rises in price because the higher interest rate more than offsets the impact of the price decline. This should seem obvious to everyone, but it’s not what we tend to think of when we hear that rising interest rates mean falling bond prices.

The point of this exercise is to put the risk of bonds in the right perspective. Yes, if rates rise sharply you’ll almost certainly lose purchasing power in your bonds, however, you will also earn a nominal return better than cash if held to maturity.3 But we should also remember that an aggregate bond portfolio with a constant maturity of about 7 years will not necessarily experience traumatic losses. In fact, even in our worst case scenario the 7 year bond only declines by a total amount of 9.6% at its low point.4 Over the course of our entire 14 years that constant maturity bond portfolio actually generated 2.85% per year. Not bad for a worst case scenario!

And this brings us to the primary problem with bond investing and asset allocation in general – most people don’t apply the right maturity and/or duration to their portfolios. Most of us suffer from a horrid case of short-termism. As I like to say, asset allocation is all about asset and liability mismatch. We have short-term cash flow liabilities that we try to match to longer-term assets. Most people want high returns today from instruments that are not designed to provide us with immediate returns. This results in a misuse of the instrument as a bond (and even a stock to some degree) is designed to pay its cash flows over certain periods of time. If you’re not prepared to potentially hold the instrument for most or all of its maturity then your risk of permanent loss increases substantially.

The key lesson here is simple – rising rates don’t necessarily mean you will lose money in bonds. While you might lose money in real terms if rates rise your probability of losing money in nominal terms is fairly low if you hold the instrument for its proper time horizon. In either case (rising rates or continued low rates), buying the appropriate bonds in a diversified portfolio is still a perfectly suitable approach for the investor who constructs their portfolio properly and within the scope of their risk profile.

¹ – A lot of people argue that individual bonds are safer than bond funds, however, this isn’t exactly accurate. Individual bonds expose you to significantly more individual entity risk and as I’ve shown here, a constant maturity bond fund is just as safe as an individual bond when it’s held for the right holding period. Unfortunately, the liquidity of bond funds often lures the investor into treating this long-term instrument as a short-term instrument. In fact, I’d argue that the ability to see your daily price fluctuations in bond funds significantly increases the behaviorally induced risk of short-termism in bonds.

² – I used a 7 year constant maturity bond because that’s pretty close to the Barclays Aggregate Bond Index. Of course, if you own a longer duration bond portfolio these numbers will not look nearly as friendly. I also assumed you were buying and holding this portfolio which is not realistic given that many investors will be contributing or reinvesting interest payments.

3 – “Cash” in this example is a 0% note and not a Treasury Bill or other risk free short-term interest bearing note.

4 – Some people might argue that this is a good argument in favor of holding individual bonds, however, I would disagree and argue that this is not a flaw in bond funds, but rather a misunderstanding of how they reflect an investor’s goals. The individual bond holder would have to repurchase new individual bonds every year in order to maintain the same constant maturity portfolio. This would result in greater single entity risk, higher costs and lower average returns. It should also be noted that the 7 year individual bond purchaser only holds a 7 year bond for a brief instant in time. After all, as time goes on that bond slowly becomes a 6 year bond, 5 year bond, 4 year bond, etc.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.