More from the “2013 was the year of behavioral finance” file…this time, some interesting food for thought from the latest Mauldin letter:

“If we look at recent years in light of long-term valuations and market behavior, we see that the combination of high and rising valuations, low and suppressed volatility, and a relatively weak trend in real earnings growth is a proven recipe for poor long-term returns and market instability.

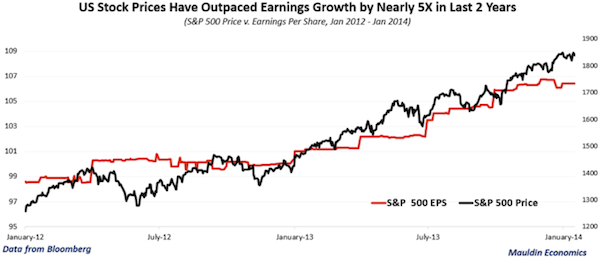

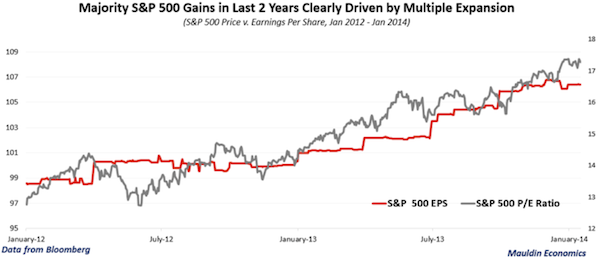

The S&P 500 Index returned 32% excluding dividends from January 1, 2012, through January 17, 2014. Over that time frame, real earnings grew by less than 8%…

… while the trailing 12-month price-to-earnings multiple has expanded by nearly 30%, from 12.8x to 17.3x.

That means most of the recent gains in US equity markets have been driven by multiple expansion, in spite of sluggish real earnings growth. Despite an improvement in the real earnings trend since I dug into US stock market valuations, multiple expansion, and earnings last August, the disproportionate amount of gains attributable to multiple expansion versus gains attributable to earnings is a clear sign that sentiment, rather than fundamentals, may be the dominant force driving the markets higher.”

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

Comments are closed.