First of all, thanks for the kind words many of you had in the comments on the open forum post. That was totally unnecessary and not what I expected. But it doesn’t go unnoticed. I have learned a huge amount from the readers here and it’s been such a delight to be able to bounce ideas off very smart people and help where I can. That said, there were a few comments and questions that I wanted to follow-up on.

Aaron: You mentioned you have no clue what’s happening in the market now. I responded that’s what trend following is for, so we don’t have to know, just follow the trend.

CR: I don’t mind trend following approaches. In fact, I think there’s a lot to learn from Trend Following. After all, I wrote the foreword for Michael Covel’s book on Trend Following! But I take a bit of a different approach even though I embed some trend following techniques into my views. I start with a fundamental macro view of the world and work down. And I funnel that into an active & passive multi-strategy approach that achieves a number of different things: 1) it automates my approach to some degree which takes me out of the game; 2) It’s designed to perform in a way that I don’t NEED to know what’s going on all the time; 3) It adheres to what I believe are the most fundamental principles of portfolio construction. So, trend following is fine, but it’s just not as all-encompassing as I believe my approach is. But like Michael Covel, will tell you, there are no holy grails!

barak: Cullen, i was wandering how MR views purchasing of fx by central banks in order to devalue the currency? Is this money printing?

CR: I don’t think this is so much a MR view as it’s a general understanding. When a central bank buys another currency they’re essentially engaging in off-balance sheet deficit spending. It can certainly be inflationary.

CR: Reader “R.D.” was screaming about me being a “neo-Keynesian”. Actually, MRists aren’t anything. At times I have very Austrian views, Keynesian views, supply side views, monetarist views. I always say “it depends”. I’ve looked like a Keynesian in recent years because of the balance sheet recession understandings, but as I’ve said to others, I was more like a supply sider in the 2005 period where I thought the government should be doing more to constrain the housing bubble. That’s the nice thing about MR – we’re not labelled as anything because we can approach any environment as its own unique experience and come to whatever policy conclusion we want based on our understandings of the monetary system.

Raskolnikov: 1–Where do you think the 10-year UST would be without QE?

2–How are the Fed’s MBS purchases effecting rates?

3—Isn’t there a danger that the economy will slide into recession due to the sequester ($85 billion) cuts?

CR: 1) I think rates would maybe be a bit higher than they are today. But the primary driver of rates, in my opinion, has been the Fed’s ZIRP and not QE. We know this because once the Fed finished QE2 interest rates actually fell. So the impact on rates seems trivial to some degree.

2) Buying MBS is forcing investors out of some bonds and into others. So it’s mostly a portfolio rebalancing effect.

3) I think the impact of $85B in cuts is overstated. Not only are we seeing private investment pick-up, but $85B is a drop in the bucket considering the economy is $16T in size.

Jaymaster: What’s the deal with all this “flexible hose” stuff I’m seeing? There are commercials on every TV channel 24/7, spam in all my email accounts, and even radio ads!

CR: I don’t know, but they look pretty awesome. I have a major pet peeve with cords, wires and things that get knotted up. My brain explodes every time I have to deal with something like that. Hoses are no exception. I saw one of these infomercials the other night and almost bought one. Your note reminds me to put it on the to-do list. I’ll let you know how it works.

Rich R: what is there to prevent a complete collapse of the banking system for the average bank customer…?

CR: Well, we rely on everyone to some degree. We rely on bank customers not to take out loans they can’t afford, bankers to prudently issue loans, investment bankers not to securitize loans they can’t afford, regulators to actually regulate banks, the Fed to be prudent, etc. The key players here are obviously the banks and the Fed. So, to some degree, we’ve outsourced the security to bankers who work purely for private purpose and an entity that is supposed to work for the government, but ends up having to work for the banks because that’s how they implement policy. It’s kind of a mess in a lot of ways, but I am not sure what the alternative is. The whole Fed system with market based money distribution via private banking is brilliant in a lot of ways, but incredibly fragile for others.

JT26: Could you expand MR a bit on the importance of capital? E.g. possibly …

– intellectual capital (nice to see these reported now as investments!)

– corporate (ex-financial) capital … esp. as it relates to Abenomics

CR: Sounds like something worthy of a full post.

Kid Dynamite: I would like to hear you talk more about Kyle Bass’s Japan thesis… he keeps talking about a pending crisis, but I get the feeling you disagree…

CR: I think Bass is wrong on Japan, but this too is probably good for a full post. These posts might wet your appetite:

https://pragcap.com/kyle-bass-its-the-beginning-of-the-end-for-japanese-bonds

https://pragcap.com/japan-isnt-bankrupt

https://pragcap.com/how-long-do-we-have-to-wait-before-wrong-is-wrong

brazzo: what is it about the financial markets community? I mean professionals working at investment banks, I’ve worked over ten years on these banks and I just can’t get rid of the impression that people working there (mostly) are so self indugent, prepotent, arrogant!!

CR: Call me. I’ll change your opinion. 🙂

Adam2: Hey Cullen, I’d like to know your and others fitness regime.

CR: 2013 has been the year of the triathlon for me and I am loving it. As I get older I’ve stopped heavy weight lifting as much as I used to. I still lift weights two or three times a week, but not like I used to….I also try to run less because it’s bad for the knees and ankles. I’m still a pretty young guy, but I’ve had a lot of sports injuries over the years so the old body is starting to fall apart fast. I have to think ahead so I can stay mobile!

That said, I am loving the triathlons for a few reasons:

1) Signing up for a race creates a sense of urgency and a deadline. I create very specific time goals for myself so if you’re not ready on race day you embarrass yourself.

2) I post my workouts publicly for people to see. Having others audit your workouts is like being forced to open the books on your business every day to a third party. It’s liberating, but also drives you to work that much harder because you know other people are watching.

3) It mixes things up. I can run 6 miles tomorrow, bike 25 the next day and swim a mile the next day. Sometimes I do all three in one day or just two. It keeps it interesting. Plus, the swimming and biking are so good for you and much easier on your body than being a full-time runner.

4) Triathletes get better with age. One cool thing you’ll notice at triathlons is that the 60 year olds can compete with the 20 year olds. A lot of it’s about mileage and the old guys have the mileage that is required to sustain yourself through a long race. So, I look forward to getting old in this sport.

That said, I don’t have a specific schedule since my schedule is always sort of building. I am running in my first olympic distance race later this summer and hope to do a half ironman next year. If things go well, I’ll be running in a full next year as well.

Aaron: On a more practical note, what does your daily schedule look like?

CR: Depends on the day. The bottom line is that I work A LOT. I’m a big believer in the idea that ambition trumps most everything else. If you really want something you’ll make the time for it. Having an orderly schedule isn’t as important as having the drive to get things done. Of course, organization helps, but being organized won’t automatically lead to results.

Boston Larry: Cullen, is the current streak in the S&P 500 one of the longest in history without a 5% correction?

CR: I believe I read Jeff Saut say that this was the third longest streak without a 5% correction. But don’t quote me on that….

Steve Roth: Cullen, I’d be very interested to hear your thoughts on this:

https://effectivedemand.typepad.com/ed/

CR: Never heard of that. Care to elaborate? I’d need some time to do a deep dive into it. Looks like fairly sophisticated modelling there….

Frederick: I’d also be interested in more of “what makes you tick”.

CR: Well, let’s not get crazy. It’s not like I’ve accomplished that much. I’m just hungry to understand how things work. That’s the big thing. I have a curiosity that drives me. I am a little OCD about the things I enjoy so I guess that helps too….

Undergrad: Any chance you could extend a MR framework to the international stage and share your thoughts on portfolio construction/risk management.

CR: Yes. Working on it!

CR: Bruno V asked about an article on the equity risk premium. I see far less value in this indicator than most others do. For instance, the ERP was elevated throughout most of the 70’s and that was a terrible time to buy equities. Then it collapsed in the early 80’s which was a fantastic time to own stocks. It remained low all through the 90s. So I don’t see how anyone can necessarily state that there’s a good correlation between this index and future returns. At best, it looks mixed.

David: 1. Am I wrong in believing that the financial community has effectively bought their own bullshit (about QE)? 2. Do you know of any cointegrative relationships between Treasury yields and the S&P 500′s earnings/dividend yield? 3. Does it also seem reasonable that the Fed could raise short-term interest rates while maintaining their asset purchase program?

CR: 1) YES! 2) No. 3) Yes, they pay IOR so it’s plausible that they could maintain or even increase the size of their balance sheet AND raise the IOR which is now the de fact Fed Funds Rate.

CollegeKid: If you were to take one entry level job out of undergrad, what would it be and why?

CR: Find someone smart who you want to work for and learn as much as you can as fast as you can.

ReturnFreeRisk: The kind of market action in the stock market reminds me of 1999. what say you?

CR: The worst market declines occur inside of recessions. I don’t see it yet. So, I am and have been a cyclical bull.

jwr: I have the Ducks in our playoff pool. If they make it to the finals I’ll have a great shot at winning the pool. Will they make it to the finals?

CR: The Capitals will win the Stanley Cup. There’s no point even debating it (I grew up in DC). 🙂

Pete: Anyone has a good explanation those broker houses such as JPM, BAC, MS have perfect trading days in a quarter? These are the market makers in any market.

CR: It’s easy to make a profit every day when you’re just scraping fees!

RB: If you could enact (or repeal) one policy to increase employment, what would it be?

CR: I’m biased, but I would cut a huge number of govt programs and start my Innovation Initiative.

John Warner: What policy changes or actions would you implement to give the US full employment, i.e., any one who wants to work will be able to find a job?

CR: I’ve mentioned no several occasions that I am not totally against scrapping unemployment benefits and replacing them with MMT’s Job Guarantee on some smaller scale to see if it would work. To me, paying people to do something is far better than paying them to do nothing. So lets’ give it a try.

Pafka: Does anyone have an idea what would be the next bubble?

CR: I have no idea, but if I were an investor in Japan I would be incredibly frightened.

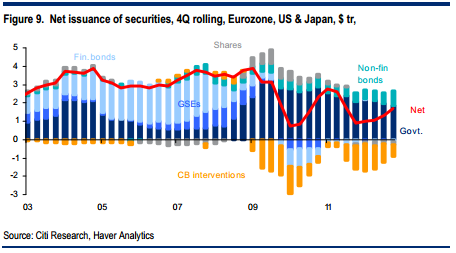

Dennis: I want to understand this chart.

https://pragcap.com/wp-content/uploads/2013/04/assets.png

{kind=link}

CR: That chart is just securities issued. It’s basically showing that most of the security issuance prior to the bubble was from the GSEs and the banks and has since become govt issued securities though that’s been largely offset by the Fed. The net is a lack of investible assets compared to the historical levels….

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

Comments are closed.