Over the course of the last 7 years there have been a series of excuses for why bad inflation predictions turned out to be bad. The most prominent excuse is that the bad inflation predictions weren’t wrong, but merely haven’t been right just yet. This is a classic move in economics. If you want to ensure that you’ll never be wrong you make a prediction, but never apply a time line. That way you can always kick the can on your prediction and say you haven’t been wrong, but merely early. This is a wonderful way to go bankrupt in the financial markets and is often a strategy utilized by morally bankrupt economists.

The most common theory about the lack of inflation with QE is the Liquidity Trap theory. This is the theory that cash and bonds have become near perfect substitutes and that the holders of these assets are relatively indifferent to them. So the demand for money is high for various reasons. This is partially true, but not for the reasons that so many people cite.

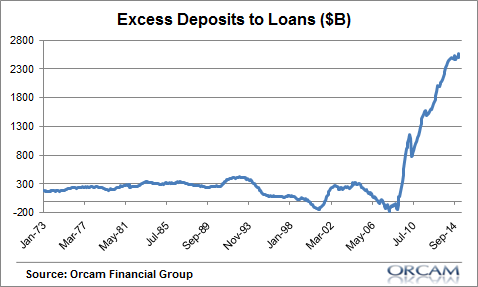

During a deleveraging cycle money is actually destroyed as loans are repaid. Just as loans create deposits the repayment of loans destroys deposits. A popular chart with the fear crowd in recent years is the excess deposit chart shown below. This chart shows the quantity of deposits that have been created via QE that were not matched by loan growth. In other words, this chart shows you how much the Fed has offset the deleveraging via QE.

But the proper way to think about this is that all the Fed did was maintain the prior trend in deposit growth. So, consider the alternative environment in which the Fed doesn’t remove T-Bonds from the private sector AND deposit growth continues at its pre-crisis trend rate. In that case we wouldn’t have had the deposit destruction from the deleveraging (it would have been deposit growth) AND the private sector would still be holding the bonds. Instead, all QE did was offset the deleveraging that would have otherwise been hugely deflationary and remove trillions in bonds from the private sector. So yes, the demand for money has been high, but it has been high because the household sector has been busy deleveraging. And all the Fed did was keep them running in place rather than sprinting forward as many in the “money printing” crowd might have you believe.

The inflation is all in stock prices, right? This is the most common retort about where the inflation went. The theory is that it hasn’t gone into consumer prices because it’s all gone into stock prices. But this doesn’t tell the full story. Yes, it’s true that the supply of bonds has been reduced which has created a portfolio rebalancing effect thereby increasing demand for other assets. But the key to rising stock prices in the last 7 years has been a boom in corporate profits, not QE. After all, just ask yourself what would have happened if corporate profits had continued to sink like a rock after 2009. Would the rally in stocks really have been all that sustainable even with QE? I seriously doubt it.

The velocity of money is low and set to rise. The velocity of money is a concept based on an accounting tautology. If you have Money Supply M, Velocity V, Price P and Output Q in MV = PQ and M is doubled, but P and Q don’t budge then do the math on V. It has to decline by half. It doesn’t tell you anything about causation. In fact, if you don’t even calculate M correctly, as this equation generally doesn’t, then it doesn’t tell you much about anything. It’s little more than another construct utilized by some economists trying to simplify a complex financial system down into one neat little (useless) mathematical equation.

Interest on excess reserves is keeping banks from lending. This was a popular one back in 2009 when economists couldn’t explain why the Money Multiplier was broken. Countless famous economists came out trying to explain the ineffectiveness of QE by claiming that the payment of interest on excess reserves was keeping banks from lending. But this is also misleading as banks don’t lend their reserves. Those who understood that the money multiplier was a myth knew that QE wouldn’t lead to more lending because banks don’t multiply their reserves when they make new loans. In addition, there’s no reason why the payment of interest on reserves would keep banks from lending to creditworthy customers. Banks are in the business of maximizing the spread on their assets and liabilities. One of the primary ways to do this is to charge high rates of interest on new loans. If a bank can lend at 4% to a safe customer it is not going to forgo this risk in favor of a very low risk 0.25% interest payment from the Federal Reserve. The problem again was a deleveraging and a lack of creditworthy customers, not the payment of interest on excess reserves.

The real problem with QE and its ability to cause inflation is none of the above. The reason why QE hasn’t resulted in high inflation is because it does not have a powerful transmission mechanism through which it can directly impact private sector balance sheets. The current asset swap program simply changes the composition of the private sector’s balance sheet and relies on various side effects (like wealth effects) to filter through the economy. These side effects alone are clearly not enough to cause surging consumer price inflation and I am quite confident that we don’t have to worry about some lag effect from QE here. 7 years should be long enough for us all to begin questioning the logic of so many of these flawed arguments.

Related:

- The Bank of England Debunks the Money Multiplier

- Understanding QE (White paper)

- The Basics of Banking

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.