I have a general theory about how good business operators think about their businesses:

“All business owners think their business is a value and growth business.”

What I mean by this is that entrepreneurs and good business owners pretty much always believe their business is selling below its intrinstic value and will provide growth in the future. I’ve run a number of businesses throughout my life and I never once said to myself “I will start a business that will only provide value and not growth!”. That’s just not how entrepreneurs and business operators think. They almost always think their business will grow and that other people undervalue that growth.

The point I am making is a relatively simple one – when someone starts a business they generally think they’re capturing an opportunity that the market has not valued properly. But this mentality does not really change as the business matures. In fact, if you look at stock buybacks you’ll notice that even very mature companies consistently believe their businesses are undervalued (sometimes even when they’re on the verge of collapse). This isn’t naive or necessarily stupid. It is the way it should be. A good business operator should always believe that their business is going to provide much more value and growth in the future than most people expect. So, I would argue that running a business is perfectly synonymous with value and growth investing.

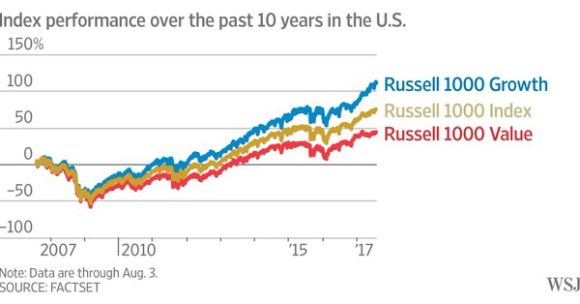

I was thinking about this as I read this article about how “value” investing has failed over time. You probably know the story by now. This group of stocks that we call “value” has underperformed “growth” and the broader market:

But let’s think this through logically. If you understand what I’ve described above then it makes zero sense to describe some companies as “value” while others are just “growth”.¹ After all, a mature company whose highest growth has probably passed them by does not simply stop trying to grow at all. And they don’t automatically become a good “value” just because they are mature. No, the operators still think they’re a growth firm that can provide tremendous value in the future. If they didn’t believe this then they would be fired.

But here’s what happens with all of this – investment managers come in and brand these companies certain things. This usually happens after an academic or researcher discovers that a certain “factor” drives performance. But factors do not describe the inherent operations of a business. They are designed to imply that the academic or investment manager knows the difference between a firm that is, for instance, “value” or “growth” (more importantly, what WILL be “value” or “growth”). And this implication is inferred because the researcher has to publish research and the manager wants you to pay them higher fees because you might think that they can provide excess return because they can identify something you can’t. The problem is, we know that investment managers stink at picking the best value or growth stocks. We also know they stink at picking when these “factors” will perform well and when they won’t.

The key point I am making is that good business operators should never just say their firm is a “value” firm or a “growth” firm. They are ALWAYS running their business as if it’s undervalued and growing.² So all of this begs the question – if a good business operator always thinks of their firm as a good value and future growth opportunity then why do we fall for the marketing pitch that investment managers sell when they imply that they know more about these entities than the actual people who run them? Said simply, when it comes to picking which stocks to own why do we still waste fees and effort guessing between the blue line and the red line when we know we can reduce the risk of owning the red line by simply owning the yellow line?

[Raises hand to answer his own question] – it’s because investors are greedy for market beating returns (guessing when they should own the blue line) and investment managers rely on charging high fees in exchange for promises they can’t deliver (pretending they know when the blue line will beat the red line). What the investors don’t realize when they buy the total market index (the yellow line) is that they already own a bunch of companies that are value AND growth firms. After all, as I described above, that’s what any successful business is and should always strive to be.

¹ – Please spare me the academic “3/5 factor” mumbo jumbo about how some Nobel Prize winner ran a backtest of results and discovered what “drives” business growth. And doubly spare me the idea that these factors can be identified in the future.

² – When the Wall Street investment manager tells the “growth” company CEO that their firm is just a “growth” company the “growth” company CEO is likely to respond by saying, “piss off, we are an extremely good value at these elevated market levels”.

When the Wall Street investment manager tells the “value” company CEO that their firm is just a “value” company the “value” company CEO is likely to respond by saying, “piss off, we will provide tremendous growth for our investors in the future”.

NB – We should dump the words “value” and “growth” (along with words like “efficient”, “alpha”, “beta”, etc.) in the big pile of Wall Street marketing terms that cause a lot more confusion than clarity. This is by design after all. If investment managers can keep you confused then they can keep you thinking that you need them to manage your money and pay them high fees.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.