John Oliver had a provocative piece on last night’s show about US auto loans referring to it as the next 2008 subprime crisis. Specifically, he compares it to the “medium short” as opposed to the “big short” because the auto loan market is small relative to the total economy. But this comparison is still overstating the size of the risk here.

We have to be really careful when comparing things to 2008 because the financial crisis was centered around the household sector’s largest asset – housing. Over the years we’ve seen all sorts of comparisons to 2008 ranging from student loan debts to muni bonds (both of which I also smacked down in real-time). These comparisons always make for a thrilling prediction, but the housing bust was an outlier event that won’t soon be repeated because of its incredible size and scope within the housing market. So let’s put this one in the right perspective.

First, the blue bars in the chart below represent the size of US consumer auto debt relative to outstanding debt. At 9% of total debt the auto loan segment is significant, but the mortgage market is 7.5X larger at 68%. In other words, the auto loan market isn’t just the “medium short”. It’s more like the “mini mini short”.

You’ll also notice something interesting in this chart. While auto loans have grown from 6% to 9% of outstanding debt in the last 10 years they look nothing like the mortgage segment which boomed from 6.3T in 2000 to almost 15T in 2007. For comparison, the recent run-up in auto loans from $700 billion in 2010 to the current level of $1.1 trillion is not remotely comparable to the growth we saw leading up the housing bubble.

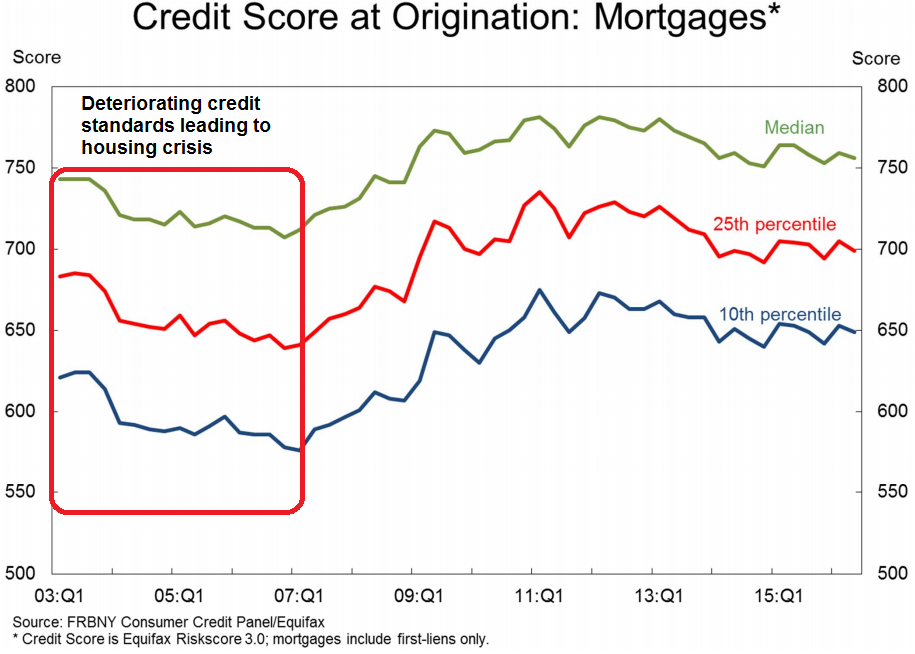

Further, the median credit scores on these auto loans have not deteriorated much in recent years. And when compared to the loosening of standards witnessed in the run-up to the financial crisis the two environments don’t look very similar:

Lastly, while securitization is a concern on Wall Street we have to keep in mind that the securitization of the auto loan market is just 1/7th the size of the mortgage market at its peak in 2007. This data clearly shows that the risks in the auto loan market are not remotely comparable to the risks we witnessed leading to the financial crisis. And while some banks and households will inevitably run into troubles during the next recession as incomes can’t service these growing debts, we should be careful about comparisons to 2008. This segment of the debt market might cause some issues in an economic downturn, but it is not the next 2008.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.