I liked the way John Mauldin described the anatomy of a bubble in his latest letter:

Anatomy of Bubbles and Crashes

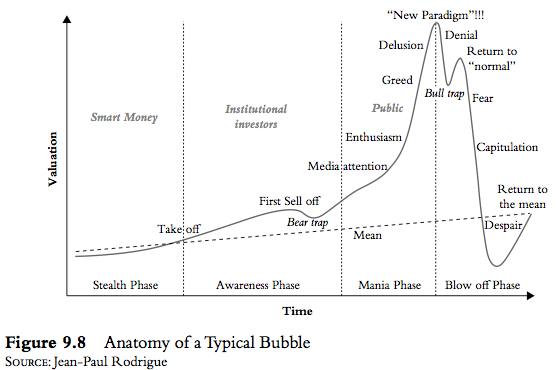

There is no standard definition of a bubble, but all bubbles look alike because they all go through similar phases. The bible on bubbles is Manias, Panics and Crashes, by Charles Kindleberger. In the book, Kindleberger outlined the five phases of a bubble. He borrowed heavily from the work of the great economist Hyman Minsky. If you look at Figures 9.7 and 9.8 (below), you can see the classic bubble pattern.

(As an aside, all you need to know about the Nobel Prize in Economics is that Minsky, Kindleberger, and Schumpeter did not get one and that Paul Krugman did.)

Stage 1: Displacement

All bubbles start with some basis in reality. Often, it is a new disruptive technology that gets everyone excited, although Kindleberger says it doesn’t need to involve technological progress. It could come through a fundamental change in an economy; for example, the opening up of Russia in the 1990s led to the 1998 bubble or in the 2000s interest rates were low and mortgage lenders were able to fund themselves cheaply. In this displacement phase, smart investors notice the changes that are happening and start investing in the industry or country.

Stage 2: Boom

Once a bubble starts, a convincing narrative gains traction and the narrative becomes self-reinforcing. As George Soros observed, fundamental analysis seeks to establish how underlying values are reflected in stock prices, whereas the theory of reflexivity shows how stock prices can influence underlying values. For example, in the 1920s people believed that technology like refrigerators, cars, planes, and the radio would change the world (and they did!). In the 1990s, it was the Internet. One of the keys to any bubble is usually loose credit and lending. To finance all the new consumer goods, in the 1920s installment lending was widely adopted, allowing people to buy more than they would have previously. In the 1990s, Internet companies resorted to vendor financing with cheap money that financial markets were throwing at Internet companies. In the housing boom in the 2000s, rising house prices and looser credit allowed more and more people access to credit. And a new financial innovation called securitization developed in the 1990s as a good way to allocate risk and share good returns was perversely twisted into making subprime mortgages acceptable as safe AAA investments.

Stage 3: Euphoria

In the euphoria phase, everyone becomes aware that they can make money by buying stocks in a certain industry or buying houses in certain places. The early investors have made a lot of money, and, in the words of Kindleberger, “there is nothing so disturbing to one’s well-being and judgment as to see a friend get rich.” Even people who had been on the sidelines start speculating. Shoeshine boys in the 1920s were buying stocks. In the 1990s, doctors and lawyers were day-trading Internet stocks between appointments. In the subprime boom, dozens of channels had programs about people who became house flippers. At the height of the tech bubble, Internet stocks changed hands three times as frequently as other shares.

The euphoria phase of a bubble tends to be steep but so brief that it gives investors almost no chance get out of their positions. As prices rise exponentially, the lopsided speculation leads to a frantic effort of speculators to all sell at the same time.

We know of one hedge fund in 1999 that had made fortunes for its clients investing in legitimate tech stocks. They decided it was a bubble and elected to close down the fund and return the money in the latter part of 1999. It took a year of concerted effort to close all their positions out. While their investors had fabulous returns, this just illustrates that exiting a bubble can be hard even for professionals. And in illiquid markets? Forget about it.

Stage 4: Crisis

In the crisis phase, the insiders originally involved start to sell. For example, loads of dot-com insiders dumped their stocks while retail investors piled into companies that went bust. In the subprime bubble, CEOs of homebuilding companies, executives of mortgage lenders like Angelo Mozillo, and CEOs of Lehman Brothers like Dick Fuld dumped hundreds of millions of dollars of stock. The selling starts to gain momentum, as speculators realize that they need to sell, too. However, once prices start to fall, the stocks or house prices start to crash. The only way to sell is to offer prices at a much lower level. The bubble bursts, and euphoric buying is replaced by panic selling. The panic selling in a bubble is like the Roadrunner cartoons. The coyote runs over a cliff, keeps running, and suddenly finds that there is nothing under his feet. Crashes are always a reflection of illiquidity in two-sided trading—the inability of sellers to find eager buyers at nearby prices.

Stage 5: Revulsion

Just as prices became wildly out of line during the early stages of a bubble, in the final stage of revulsion, prices overshoot their fundamental values. Where the press used to write only positive stories about the bubble, suddenly journalists uncover fraud, embezzlement, and abuse. Investors who have lost money look for scapegoats and blame others rather than themselves for participating in bubbles. (Who didn’t speculate with Internet stocks or houses?) As investors stay away from the bubble, prices can fall to irrationally low levels.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.

Ralph Hinkley

Back in 2011 you wrote an article that we don’t have to worry about the exploding money supply because loans were not exploding… since they have set a steep growth curve since middle of 2011, care to run an updated story on the likely impact on inflation of our growing money supply, which is being lent out at record rates now?