The latest installment from Tadas Viskantas’s series on “financial blogger wisdom” (is that an oxymoron?) asked a bunch of smart people (and also me) about smart beta. I was short:

Smart beta and factor investing are the newest versions of high(er) fee active management promising the fairy tale of “market beating” returns in exchange for higher fees and usually delivering lower returns (after taxes and fees).

Regulars know I am not a big fan of Smart Beta and Factor Investing (sorry to all my friends in the industry who love these approaches!). For the uninitiated, Smart Beta basically involves taking an index fund and changing it so it captures a “smarter” type of return. For instance, you might take a market cap weighted index fund like the S&P 500 and equal weight it so that it doesn’t expose you to the procyclical tendencies of the market cap weighted fund which will tend to be overweight the riskiest stocks at the riskiest points in the market cycle. The evidence that this is countercyclical is weak as Vanguard has shown and as I expressed in my new paper.

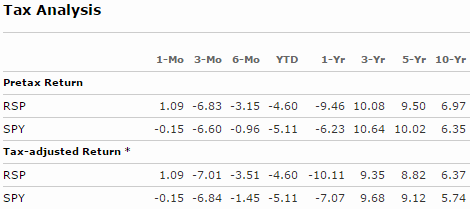

Further, you will generally pay higher taxes and fees in these funds without a high probability of better results. For instance, the equal weight S&P 500 has a pretty mixed performance versus the market cap weighted S&P as it’s performed better on a 10 year basis, but underperformed on all periods shorter than 10 years.

The nominal returns are slightly better over longer periods, but that’s only because the equal weight fund has a much higher standard deviation with 95% of the total correlation. So, the intelligent asset allocator has to ask themselves why they’d pay for 95% of the correlation while guaranteeing higher taxes and fees without a reasonably high probability of better risk adjusted performance? Should you really pay higher fees for the empty promise of “market beating returns”? I say no.

The same basic story can be laid out for factor investing. There’s a great irony in the idea that the founder of the Efficient Market Hypothesis says you can’t pick stocks that will beat the market, but you can construct index funds that will be comprised of the stocks that will beat the market. The problem is, no one knows what are the right stocks to put in a “momentum” index before they earn the momentum premium. And just like active mutual funds, no one should pay a premium for an asset manager who claims that they can construct an index that will be comprised of stocks that will benefit from “market beating” returns in the future. You just end up guaranteeing higher fees and taxes in exchange for the empty promise of market beating returns.

To me, these are just the new forms of “active” investing charging people higher taxes and fees for indexing strategies that won’t outperform.

Mr. Roche is the Founder and Chief Investment Officer of Discipline Funds.Discipline Funds is a low fee financial advisory firm with a focus on helping people be more disciplined with their finances.

He is also the author of Pragmatic Capitalism: What Every Investor Needs to Understand About Money and Finance, Understanding the Modern Monetary System and Understanding Modern Portfolio Construction.